4 Ways To Upgrade Your Financial Life Without Earning More Money

This post is brought to you in partnership with Chime.

When you first find yourself thinking, “Damn, I wish I could totally overhaul my financial life and make everything way easier,” one obvious solution springs to mind: get more money. Duh — earning more money (or somehow acquiring it through no effort whatsoever — the ultimate dream) would certainly make your life easier. Sadly, it often isn’t possible. Most of us are stretched pretty thin already. But if you don’t have another way to earn extra cash, I have good news: you don’t have to earn more money to upgrade the hell out of your financial life. In fact, most of the best financial strategies have nothing to do with making more money, and everything to do with being more mindful about how you manage the money you already have.

Speaking from my own personal experience, there are probably ways I could be earning an extra buck right now, but before I add more work on to my to-do list, I want to focus solely on growing in my new role with TFD. This means that most of my lifelong side-hustles (like childcare, which I’ve always been so deeply fond of) have been pushed to the backburner. Which is fine — except for when it’s not fine, because the loss of a side-hustle means the loss of its cash flow. Which means I’ve spent the past few months being extra mindful about how I’m handling my money, and putting a lot of energy into thinking about the choices I’m making with it. I’ve found that there are a lot of easy moves I can make to up my game, and I’m here to share them with you. With that, we partnered with Chime — a digital bank with some great savings features — to bring you four ways to upgrade your financial health (without earning any extra money).

1. Have a radical-honesty session with yourself.

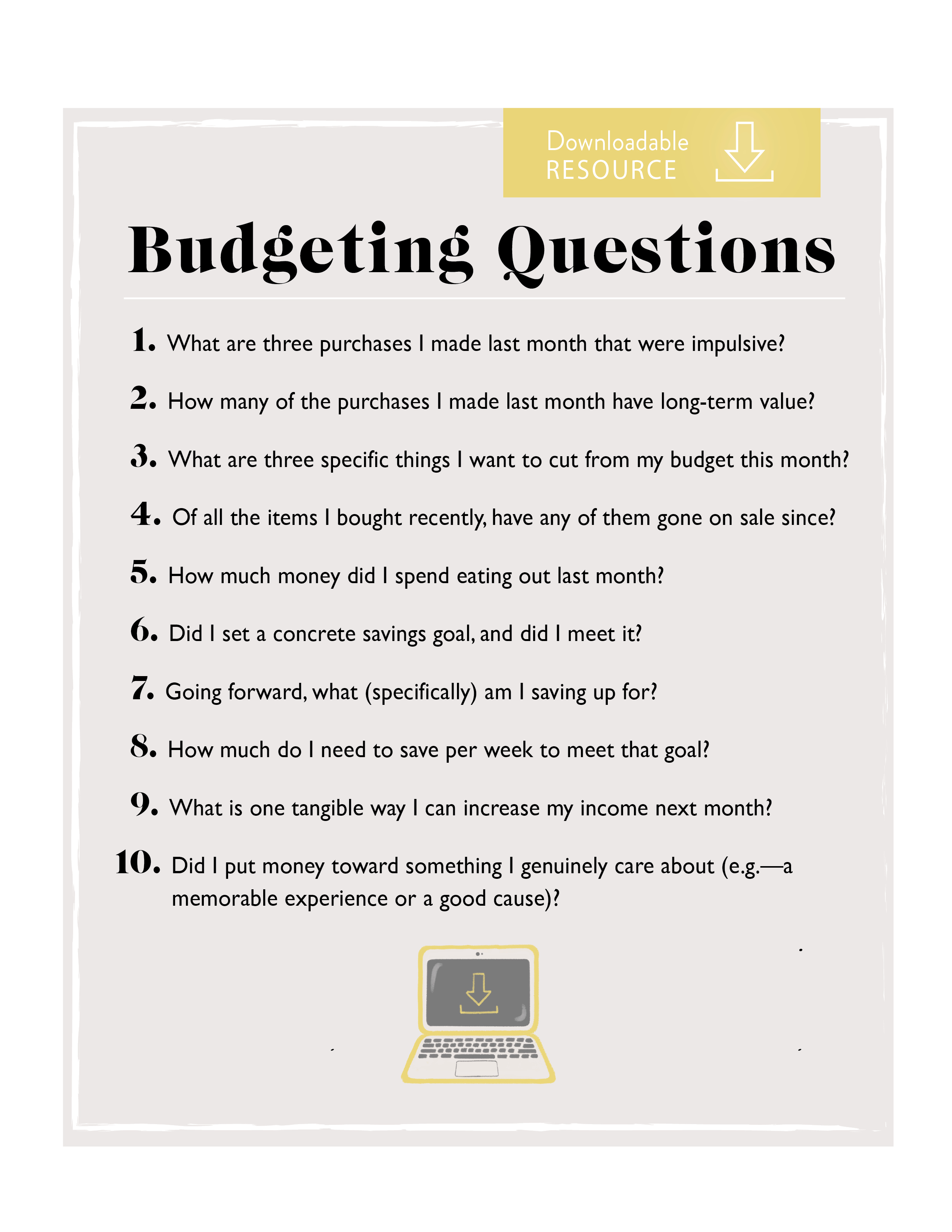

In which you sit down, preferably alone, with a printed copy of your bank statement and a highlighter, and go through every single purchase carefully. Then highlight the purchases you truly regret, or truly don’t even remember making. If you do this even once, you’ll likely notice a pattern; maybe you’re spending $8 at Starbucks every day that you can cut down to just $3 if you lighten up your coffee order or pass on getting a pastry with your drink. Maybe certain stores take tons of your money every time you go — and maybe you go to them way too much (I’m looking at you, T.J. Maxx). It’s very common to trick yourself into thinking you spend less than you do. One study found that people tend to severely underestimate how many things they buy online each month (with the actual number being double what they report).

As you take a metaphorical “pair of glasses and tweezers” to your statements (as we like to say here at TFD), notice which expenses really did and didn’t add value to your life. Did you have a totally unmemorable dinner out one night when you were feeling too lazy to cook? Cut that place out of your mind, and never go there again. The more often you practice being ridiculously honest with yourself, the less likely you are to put money in places that just don’t matter to you. This is how I learned (the annoyingly hard way) that I am not to be trusted in Target — it is essentially where I go to waste time and money on things that just don’t matter. If I go there, I absolutely need to be armed with a list, and accompanied by someone who will ensure that I don’t get off task. There’s a whole section on the TFD book in this, with a pretty little downloadable resource.

But the self analysis doesn’t have to be all negative. When looking at your spending, you’ll likely see at least a few things that did feel worth it, which will serve the dual purpose of reminding you to be grateful for all the nice experiences and things you gained, and giving you a guide for how to spend in the future. Once you’ve identified which expenses really made you happy, you can schedule more of those (for instance, a dinner with people you love, or a weekly yoga class). Even a purchase could be “scheduled” if you know in advance that, say, you need an outfit for a wedding in several weeks. If your money is already “spoken for” at the beginning of the month, you’ll have much more resolve to say “no” to impulse purchases. You could even put images of these priorities on your desktop or lock screen to help motivate you. The idea isn’t to deprive yourself — just to break lazy habits that aren’t serving you well, so you can enjoy what you do spend on more.

2. Give some love to your inbox.

I have three email accounts, and they are where all of my hopes and dreams about being a better human being go to die. If your email life is as chaotic as mine, taking a few hours one day to really go through and clean it up might be a game-changer. For your work email, go through and get rid of the clutter that is distracting you from doing your work in the most time-and-money-efficient way possible. If you’re wasting hours of your workday trying to comb through garbage emails to get to the important ones (and not starring the really important ones so they never get lost in the clutter), you’re doing yourself a disservice, and likely setting yourself up for late nights of unpaid overtime. For your personal email, go through that sneaky promotions tab and unsubscribe from everything that a) annoys you, or b) tempts you. It’s important to remember that companies pour millions of dollars into honing their email promotional campaigns, and many consider it their most effective form of marketing. By one measure, email is 40x more effective at getting people to take action than Facebook or Twitter, and people who shop via email spend 138% more than people who don’t get offers through their inbox. Proceed with caution!

You can definitely use a service like unroll.me, but personally, I like to go through my inbox and manually unsubscribe, because I actually do really value certain promotional emails and find them to be helpful in my financial life. The online store where I order cleaning supplies, for example, gets a pass, as does Old Navy, because I find everything there to be affordable and of good quality, so I frequent their site when I’m in need of clothes. However, the daily ~Flash Sale!~ emails I get from stores I don’t give a damn about but signed up for on a whim need to go. Not only will you feel less tempted, but your cleaner inbox will make you far less likely to miss or ignore important notifications from places like your bank, whose notifications you should be diligently opening and reading. Which brings me to…

3. Weigh out your banking options.

When it comes to banking, it is easy to become so settled and comfortable that you don’t even stop to question what might be costing you money, or preventing you from saving. Are there other types of savings you could be maximizing? Is your bank charging a monthly maintenance fee? Instead of stagnating, look into your situation and see what can be made better. Switching to a new bank seems like a lot of work — in fact, I never really considered it for most of my life as the owner of a bank account. That is, until a few months ago. I talked about this in another post, but I started using Chime recently as a way to save in a separate account for a summer vacation. The experience of trying a new bank when I’ve literally been using the same one my mom signed me up for when I was 15 and she thought I was #Ready for a bank account was super enlightening.

I’ve been with the same bank for years just because I never really cared to look into options out there, and I’m sure a lot of people do the same. It is easy to just become comfortable with routine, even if your routine is costing you money. But most banks have so many fees that are truly eating away at our funds every day without us even realizing it, and it is definitely worth the few minutes of effort it takes to research better options and sign up for a new bank. Chime is a bank account with no fees (except for a very small out-of-network ATM fee — but it’s easy to avoid because they have more than 38,000 ATMs). This means that if you, like me, don’t have a ton of money to put into your account, you won’t incur ridiculous “minimum” or monthly fees that stand in the way of your goals. They also have an automatic savings feature that rounds each purchase you make on your debit card up to the next dollar, and transfers that change automatically into your savings account. Sounds like nothing, but when you’re making 5+ small purchases in the day (like your morning coffee, your mid-morning coffee, your lunchtime coffee, etc., or, you know, real necessities) it really adds up. Automating savings is one of the easiest ways to make sure you’re at least putting a little slice into your savings account, even if you’re not actively deciding to go in and transfer funds over every day. Lastly, their Get Paid Early feature is an awesome way to get your money even earlier than normal through direct deposit — more time with your money = more time to manage your savings and work towards your goals!

No matter what your current banking situation is, there are likely ways you could be using your accounts more creatively, and the best way to start is just familiarizing yourself with the ins and outs of what your bank offers. Many banks have different types of saving accounts (like a Certificate of Deposit) that have higher interest rates than typical savings. You can also nickname your accounts things like “Summer Beach Trip” to remind you why you’re saving (a tactic our Thursday video host, Erin, swears by). And you can automate many recurring payments, such as utility bills (sometimes even rent) so they’re always paid on time and you don’t get slapped with surprise late fees or delude yourself into thinking you have more than you do.

4. Give yourself a financial check-up.

Just like it’s important to go to the dentist twice a year even if there’s nothing wrong with you, your financial health deserves some attention a few times a year. No matter how much you have, it’s always good to know where you stand, so you can make more informed decisions about how to manage your money going forward. Even if it gives you anxiety to do so (erm — actually, especially if it gives you anxiety to do so), give yourself a little financial check-up. Analyze your net worth (which essentially means to compare what you own with what you owe) and create an excel sheet to organize your debts and better organize your payoff plan. There are a lot of resources out there to help do this, for instance this calculator can help show you whether it makes sense to invest even if you have student debt. Investing when you’re young makes such a difference for your long term financial security that it’s worth doing even if you don’t have a ton to start with.

Beyond debt payoff and investing, it’s also good to periodically do a soft check of your credit score to see where it might have been bumped down or up a few points in recent months. If it’s not looking so great, we have an entire section on TFD about building credit with tested tips and real life stories of how our readers raised their scores. Finally, look ahead to any long-term plans you have (like buying a home or having a kid) and figure out how much you’d like to have saved just so you know what it’d take to get there. Of course, both of those figures are highly subjective but just starting the process of asking around and researching is the first step to determining how you want to approach those goals. It might inspire some awkward conversations with your partner (or self), but those are important conversations to have regardless. Living a financially healthy life isn’t just about making the most money, or even making more money than you are now — it is just about figuring out the best way to make your money work for you. You have complete power over your financial life (scary, but true — and also kind of exciting, if you ask me!) and it is up to you to streamline it in whatever way possible so it makes sense to you.

Image via Unsplash

{kind=link}