Introducing TFD’s Money Personality Matrix, & How To Determine Your Money Identity

This post is brought to you by CreditRepair.com

Here at TFD, we are a little obsessed with personality types. Sure, the Myers-Briggs identities may only tell you as much about yourself as your astrological sign, but who cares? Learning a specific personality type you identify as is simply a way to know yourself better. And when it comes to your financial life, knowing yourself better means knowing which strategies will work for you — and which really won’t.

After nearly five years of talking about money, we know that there are ample factors that influence how one person chooses to handle her finances. But while no two people treat money exactly the same, identifying your main habits and priorities — and how to use them to your financial benefit — can be immensely helpful. That’s why we’re collaborating with our long-time partners at CreditRepair.com to bring you TFD’s own money personality matrix!

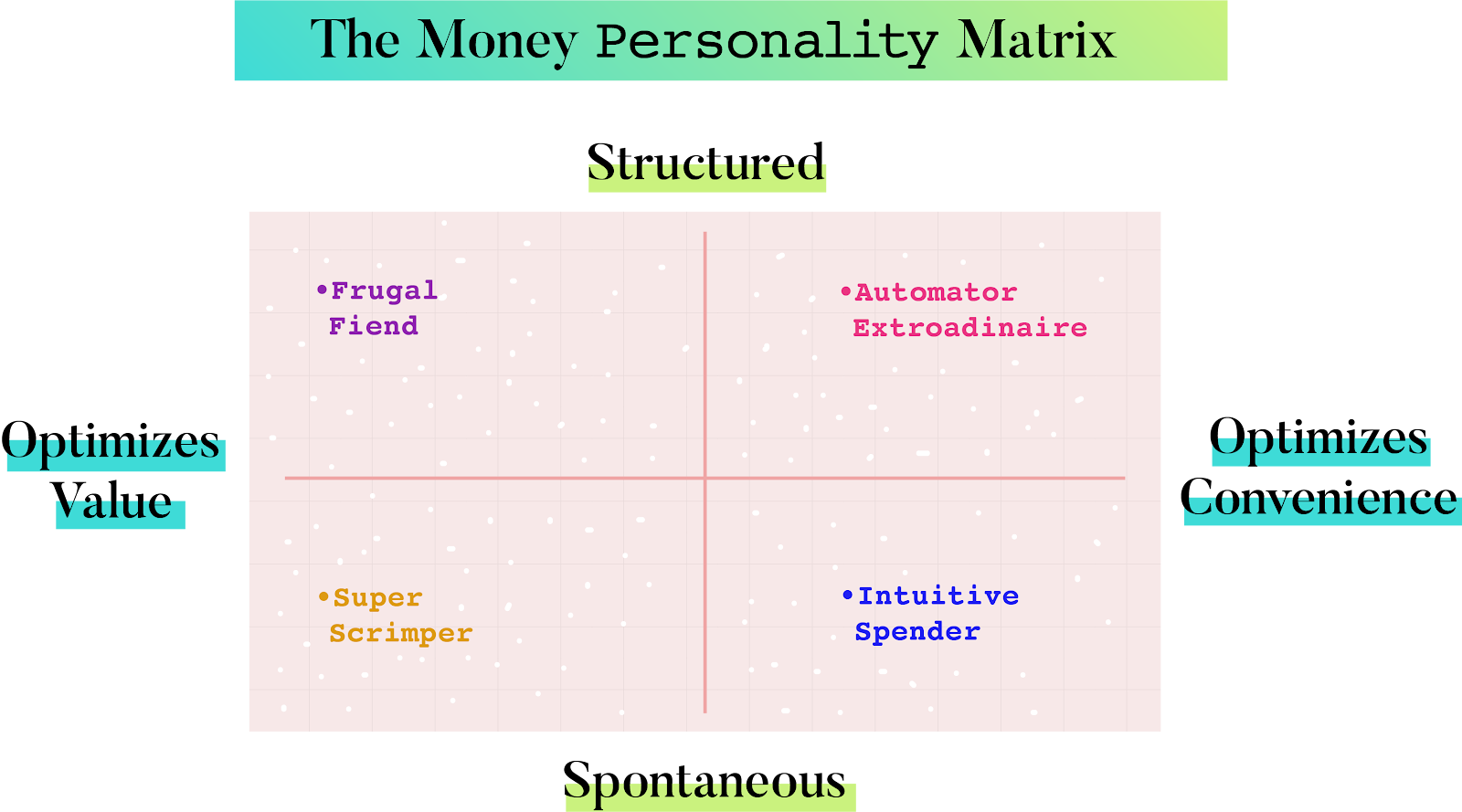

We’ve based this matrix on two specific spectrums when it comes to how people handle their finances: whether they are more structured or spontaneous, and whether they optimize convenience or optimize value. After answering the quiz questions below, you’ll be able to identify roughly where you fall on our money personality matrix:

Take some time to answer the questions below to find out your own money personality — and remember, the more honest you are with yourself, the easier it will be to put money systems in place that are right for you!

TFD’s Money Personality Quiz

1. When it comes to budgeting, you prefer to:

A. Set it and forget it. You feel most comfortable using an app to track your purchases and alert you when you’re approaching an overage in a category.

B. Get meticulous. You have a spreadsheet that allocates every single dollar you earn — and you actually look forward to your weekly budget check-ins.

C. Let it be. Whenever you’ve tried sticking to a specific budget, you always overspend, and you just give up altogether.

D. Budget for the big stuff, like living expenses, and then casually monitor the rest of your monthly spending as you go. You’re used to living frugally and don’t have to try not to go overboard.

2. What does your emergency fund look like?

A. A solid 3 months’ of expenses built up — anything more than that would be excessive at this point in your life. You’re more focused on investing any extra cash.

B. If you got in a bad accident and lost your income stream tomorrow, you would be set to survive an entire year or longer on your current budget.

C. Relatively nonexistent. You’ve always been able to cover “emergency” expenses with a credit card and pay it off eventually.

D. It may cover several months of expenses, but you haven’t checked it in a while. You’re so used to setting aside whatever’s leftover, and you avoid touching your savings at all costs.

3. Your credit score is:

A. Definitely good. You know what you have to do to keep it up, but don’t worry about it too much otherwise.

B. Freakin’ excellent. You’re super on top of payments and strategic about your credit usage, and you check your bank’s free monthly credit score update like clockwork.

C. Not sure — you don’t remember the last time you checked it.

D. Not bad, but not as great as it could be — you’re pretty debt-averse and don’t like to use credit cards, so your credit isn’t as established as other people’s.

4. Do you ever buy things on impulse?

A. Rarely — you’ve been burned too many times in the past, and you know yourself well enough to know there’s nothing you’d rather do less than going out of your way to return something.

B. Nope. Everything you buy has been meticulously thought out beforehand. In fact, it throws you off when you suddenly need to buy something you hadn’t planned ahead for in your budget.

C. Yes — you feel deprived if you don’t have the freedom to buy what you want in the moment.

D. Yes, but only small things — a super-discounted pair of earrings or a fun snack on a grocery trip.

5. What are your tactics for meal planning and grocery shopping?

A. You plan your meals ahead of time and keep plenty of snack staples in the kitchen. You’re willing to pay a little extra to go to the slightly-more-expensive store close to home, because it saves you easily 40 minutes per trip.

B. You are a meal prep pro. You spend your Sundays planning the week’s menu around your store’s available coupons, shopping, and prepping all your breakfasts and lunches for the week.

C. Even though you might love cooking, you don’t love planning ahead. You often buy ingredients for a certain recipe on a whim, but then you don’t end up using all the ingredients before they go bad. The Trader Joe’s frozen foods section is your best friend because you don’t have to worry about meals going bad before you get around to eating them.

D. You regularly stock up on inexpensive staples, and you have your favorite (and most cost-effective) takeout orders saved in your delivery app.

6. What kind of credit card(s) do you use?

A. One solid credit card for pretty much everything — it may have a not-insignificant annual fee, but the benefits and points more than make up for it. You use the autopay option to pay it off in full before the due date every month.

B. Several to a dozen cards, each with their own rewards systems that you know by heart. You use different cards for different purposes to maximize the points you can earn. And you cover the costs you put on each card as soon as they hit — no use risking making a late payment.

C. Whichever one you got a pre-approval offer in the mail for first.

D. None, really — you’re relatively risk-averse and don’t see the point in swiping a credit card for purchases you can cover outright.

Now, tally up your answers to find out your most prominent personality type.

Below, we’ve outlined the general characteristics of each money personality type, and offered tips for how individuals within each category can play to their personality type’s strengths — and weaknesses. Of course, most people won’t fall squarely into one personality type or another. The point is to get a better understanding of your innate tendencies so that you can make your money work in the way that’s best for you.

Mostly A’s: Automator Extraordinaire

The “Automator Extraordinaire” prioritizes structure and convenience. She:

- Has her savings and investments on autopilot

- Is app-savvy — she budgets digitally (rather than with a spreadsheet or pen and paper) in order to save time

- Is willing to pay extra for an expert to do pretty much anything she thinks is worth it, from credit score monitoring to investment management to a great haircut

- Avoids money anxiety by setting up ample text alerts — bank account balance checks, credit score dips, large purchase notifications, etc.

Pop culture examples: Miranda Hobbes, Mindy Lahiri

Tip: Automator Extraordinaires seem to have their financial sh*t completely together, and for the most part, they do! Just make sure you don’t get too comfortable with your current money systems. Schedule a quarterly or monthly check-in to see if you could or should be saving more than you currently are.

Mostly B’s: Frugal Fiend

The “Frugal Fiend” prioritizes structure and value. She:

- Spends ample amounts of time clipping coupons, scouring deal websites, and other ways to cut costs as much as possible

- Loves her zero-based budget spreadsheet more than pretty much anything and schedules weekly budget overviews

- Is extremely into credit card churning to maximize points

- Takes comfort in knowing exactly when every dollar comes in and where it goes

Pop culture examples: Jessica Huang, Sutton Brady

Tip: Cutting corners is helpful for so many people, but Frugal Fiends have been known to take it too far and get thrown off by even a tiny unexpected expense. If this sounds like you, try setting up a “sinking fund” to avoid the anxiety of an unplanned purchase.

Mostly C’s: Intuitive Spender

The “Intuitive Spender” prioritizes spontaneity and convenience. She:

- Doesn’t like to abide by a super-strict budget

- Has learned to say “no” to spending when she knows it’s really not worth it

- Is happiest when she can buy something on impulse without having to worry about it, whether that’s concert tickets or a must-have kitchen item

- Would rather focus on earning more than trying to spend less

Pop culture examples: Carrie Bradshaw, Alexis Rose

Tip: If you identify as an Intuitive Spender, consider using an app that allows you to save and invest your money on autopilot. That way, you can worry less about saving because you simply won’t have to think about it. “Spare change” apps are great, because they are built to transfer money to your savings when they know you won’t miss it.

Mostly D’s: Super Scrimper

The “Super Scrimper” prioritizes spontaneity and value. She:

- Is used to living on less for one reason or another — doesn’t have to try to be frugal, it’s just her nature

- Relies on apps for deal alerts and discounts; is a big believer in subscribing to store emails to get latest alerts on deals

- Will buy whatever brand is on sale at the store, but won’t necessarily research or clip coupons ahead of time

- Is somewhat wary of credit cards — she’s more comfortable paying for everything with cash or debit, so she knows she can swing whatever it is

Pop culture examples: Lorelai Gilmore, Fiona Gallagher

Tip: There’s absolutely nothing wrong with avoiding risk, but taking calculated risks can have a huge payoff. If you’re a risk-averse Super Scrimper, consider opening some sort of credit account (if you haven’t already!) to start building credit. And with CreditRepair.com, keeping tabs on your credit score can be so much easier than you think!

*****

Now, did you get the answer you anticipated? Let us know in the comments!

Think CreditRepair.com could help you? Check it out to learn how they can help you work to repair, build, and maintain your credit score by working directly with the credit bureaus to challenge any items on your credit report, and teaching you how to understand both your own score and the rating system.

Image via Unsplash